In our last blog, we started to frame the issue and disclose the undisputable numbers regarding how much healthcare costs, how many are insured/uninsured, and what the per-capita cost for healthcare is in the United States. Additionally, we talked about how attractive the idea is just to extend Medicare to all Americans.

Well, some could say that maybe it means that Medicare will be only extended to the uninsured. It is a reasonable idea to insure the 28.5 million uninsured Americans. How many companies will just drop insurance if that is the case? As a small company, we will not, although many others will consider it.

The graph below depicts flooding numbers that will use the new Medicare for All program.

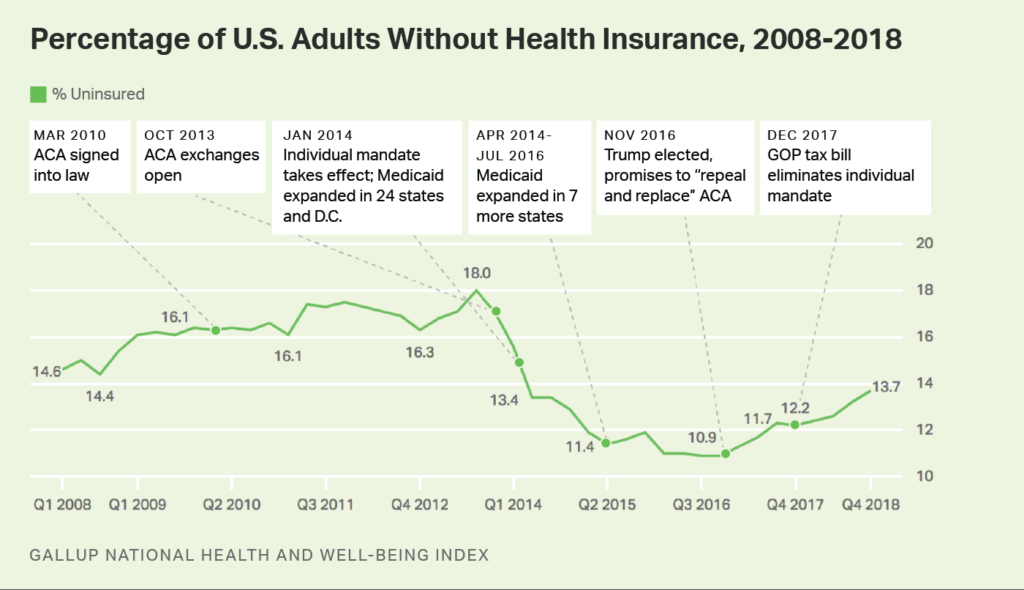

Recently, the Gallop Organization released a poll that reported, “Americans without insurance rises to 4-year high.” The finding noted 13.7% of Americans have identified themselves as uninsured (see nearby graph). The report went on to state, “women and adults under 35 had the highest rates, 12.8 and 21% respectively.” This sampling is based on random contact to 28,000 adults.

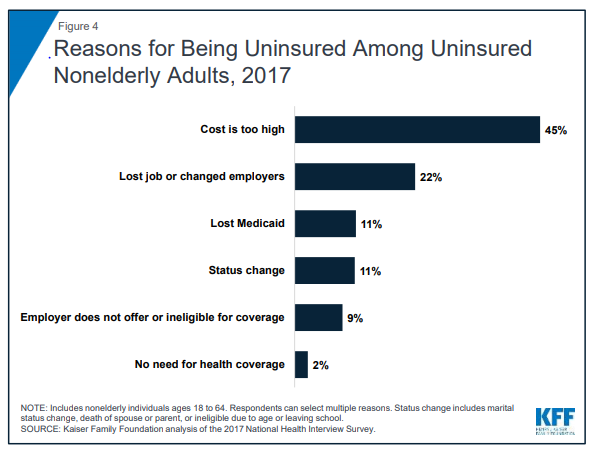

In 2017, the Kaiser Foundation did a study on healthcare and the uninsured (see nearby graph). The report, if close to accurate, said that 22% were between jobs, 22% were losing Medicaid or changing status, and 2% said they did not need it. We can extrapolate that maybe a quarter of the total uninsured are between jobs or undergoing other life and qualification status changes. We still have a lot of people that cannot pay for healthcare or health insurance, and no question about it, we need to find a way!

One of the admitted challenges with Medicare is that there are no gate keepers (for the most part). Like insurance companies, Medicare has no method to either pre-approve or redirect care – Medicare provides no direct services. As long as everything is well documented, there are no real filters in the cost or intensity of the care given. Sometimes the cost is higher because higher-end procedures are applied; when in reality, there are lower cost procedures available or at least a stepping stone to more advanced work.

In most cases, Medicare does not negotiate prices; generally, Medicare rates are between commercial insurance and Medicaid however, not always.

Most healthcare providers, including hospital, ancillary providers and doctors, at best break even on providing care on Medicare. In many cases, the cost of care exceeds the cost to provide the care.

This is not theoretical to me. We have tracked this disparity for years with historical cost accounting analysis. Why did we continue to provide the care? So long as we had more commercial insurance patients, the method works. For one, Medicare generally pays faster than traditional insurance. If you noted from our last blog, EBITDA, a non-profit hospital was a meager 1.5% of collected revenues.

Today, it is the commercially insured patient that is subsidizing traditional fee for service (FFS) for both Medicare and Medicaid. This means that there are billions of cost transfers going on today at every level of healthcare from commercial to Medicare and Medicaid.

A very recent survey of members of the Medical Group Management Association (MGMA) reported that 67% of its members (respondents) cost of providing care was higher than the payment they received from Medicare, and 17% said the costs were equivalent to reimbursement. Only 16% said they made a profit providing medical care to Medicare beneficiaries.

This leads us to question – how long can an industry provide a service if 84% of the time the cost was less than or equal to the service provided? Are we talking about putting more patients though this system? I am not surprised if the numbers are same or marginally better at the hospital level. No industry can survive under only those conditions.

One option is to increase the reimbursement to providers and hospitals. I would estimate that would require about 40-60% increase in reimbursement.

If we allow Medicare for All and do not increase reimbursement, we will see a historically unprecedented contraction in caregivers, and the failure of hundreds and thousands of hospitals.

Recently, the Mayor of New York City held a news conference promising $100 million to cover the care of an estimated 600,000 New Yorkers without insurance. Someone who has been in care delivery as long as I have been, could quickly do the math from the headline alone – calculate $100,000,000 divided by 600,000 equals $166.67 per uninsured New Yorker per year. So, relate that to the annual cost of healthcare per capita (average cost, not the higher cost in NYC) of $10,661.43.

We can quickly determine that at the best-case scenario, that huge amount of money may pay for one physical a year, and maybe some OTC medication for each of the 600,000 people. Don’t get me wrong, that is better than what they have, and it will save many lives.

We must face the facts that it will not solve the issue of 600,000 uninsured; it might help in getting people to qualify/apply for other programs like Medicaid. The take away is that the primary care component will consume the entire $100M. To have some measurable mass impact, that number will have to be close to $1 billion.

Others have told me that Canada, United Kingdom, Finland and other developed and prosperous countries have made it work, why not the United States of America?

We will discuss that in our next installment of this series.

-Noel J. Guillama, President